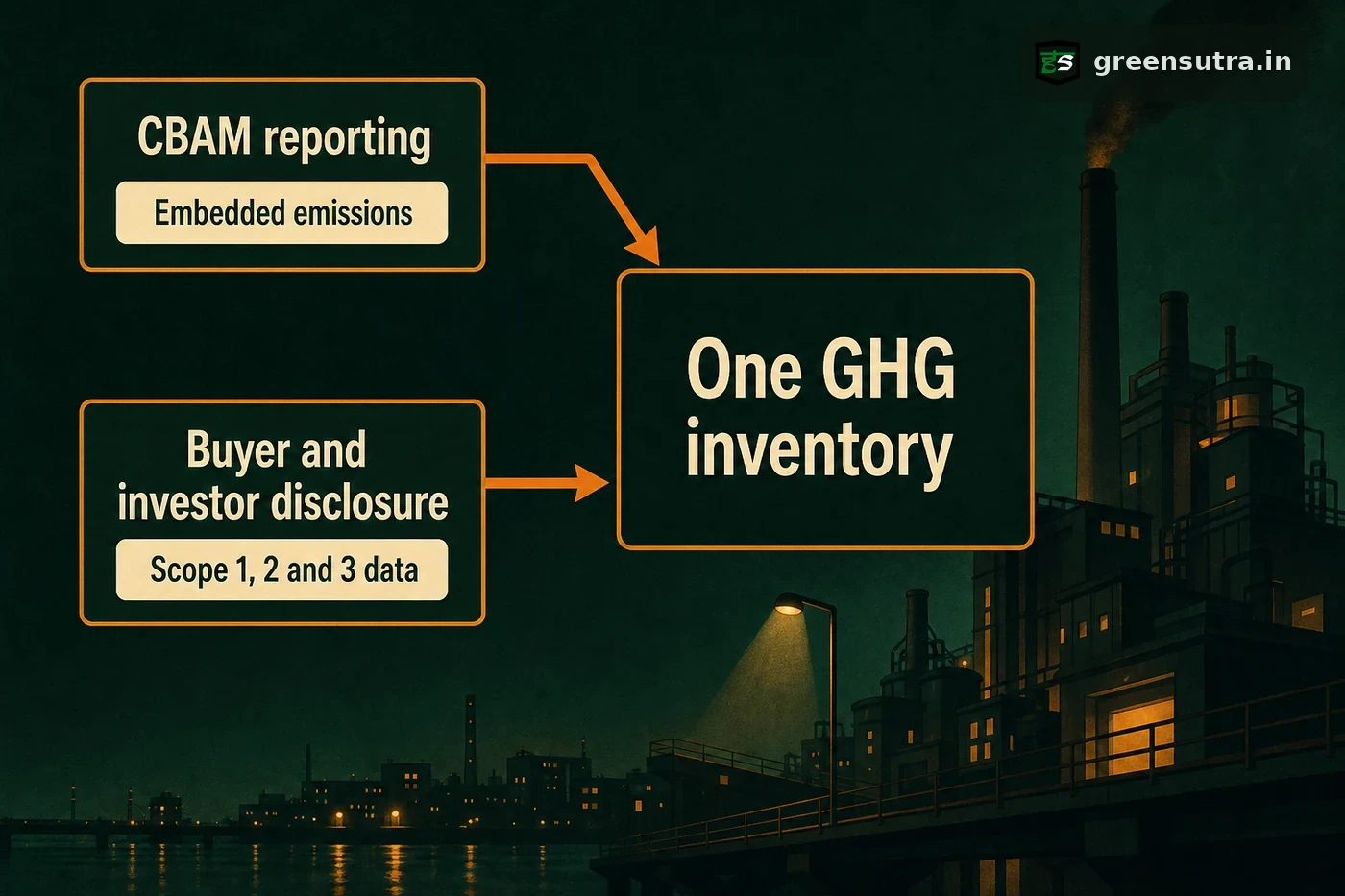

No single EU rule forces every Indian exporter to publish a carbon footprint, yet a measured footprint is increasingly needed on two fronts: exporters of CBAM-covered goods must report embedded emissions, and EU buyers and investors request Scope 1, 2 and 3 data for their own sustainability reporting. One greenhouse gas inventory answers both.

There is no single blanket requirement

Carbon footprint reporting is not imposed on Indian exporters by one universal European Union rule. The accurate position is conditional. Whether a footprint is needed depends on the goods shipped and the customers served, not on a blanket mandate that reaches every consignment.

Two live pulls, however, make a measured footprint the practical evidence base for continued access to the European market. The distinction between the two matters, because each is triggered by a different party.

| Pull | Who triggers it | What is asked for |

|---|---|---|

| CBAM reporting | EU import rules on covered goods | Embedded emissions of the product |

| Buyer and investor disclosure | EU customers and investors | Scope 1, Scope 2 and Scope 3 data |

Embedded emissions for CBAM-covered goods

Exporters of goods covered by the EU Carbon Border Adjustment Mechanism must report the embedded emissions of those goods, and the India to EU trade relationship gives no exemption from that duty. The scope of covered goods, the phase-in and the certificate mechanics sit on the CBAM consulting service, where the reporting rules are set out in full. The underlying figure is a product-level emissions value, prepared from the same activity data that an organisational Scope 1, Scope 2 and Scope 3 inventory draws on.

Scope 1, 2 and 3 data for buyers and investors

EU customers and investors increasingly request supply-chain emissions data for their own sustainability disclosure. Where a customer falls under the EU Corporate Sustainability Reporting Directive, or an investor works to ISSB-aligned standards, suppliers may be asked for Scope 1, Scope 2 and Scope 3 figures. Those disclosure thresholds and dates belong to ESG reporting and are covered on the ESG reporting guide. The request that reaches an Indian exporter is for credible emissions data, not for a particular certificate.

A single greenhouse gas inventory, quantified to the GHG Protocol, GRI and ISO 14064 across Scope 1, Scope 2 and Scope 3, satisfies both pulls at once. Carbon footprint consulting identifies the emission sources and estimates that inventory, the carbon footprint guide sets out the method, and a scoping conversation maps which pull applies to which shipment.

Sources: GHG Protocol Corporate Standard · ISO 14064-1 · GRI Standards