IFRS S1 and S2 are the ISSB sustainability disclosure standards issued in June 2023 and effective for periods beginning on or after 1 January 2024, providing an investor focused global baseline where IFRS S1 covers general sustainability related financial information and IFRS S2 covers climate and builds on the TCFD recommendations.

What the ISSB standards set out

The International Sustainability Standards Board (ISSB), under the IFRS Foundation, issued IFRS S1 and IFRS S2 in June 2023, and both apply for annual reporting periods beginning on or after 1 January 2024. Together they form a global baseline for investor focused disclosure: IFRS S1 sets general requirements for sustainability related financial information, while IFRS S2 covers climate related disclosures and builds on the recommendations of the Task Force on Climate related Financial Disclosures (TCFD). Preparing this data cleanly is the core of ESG advisory work, and one evidence base can serve several reporting formats.

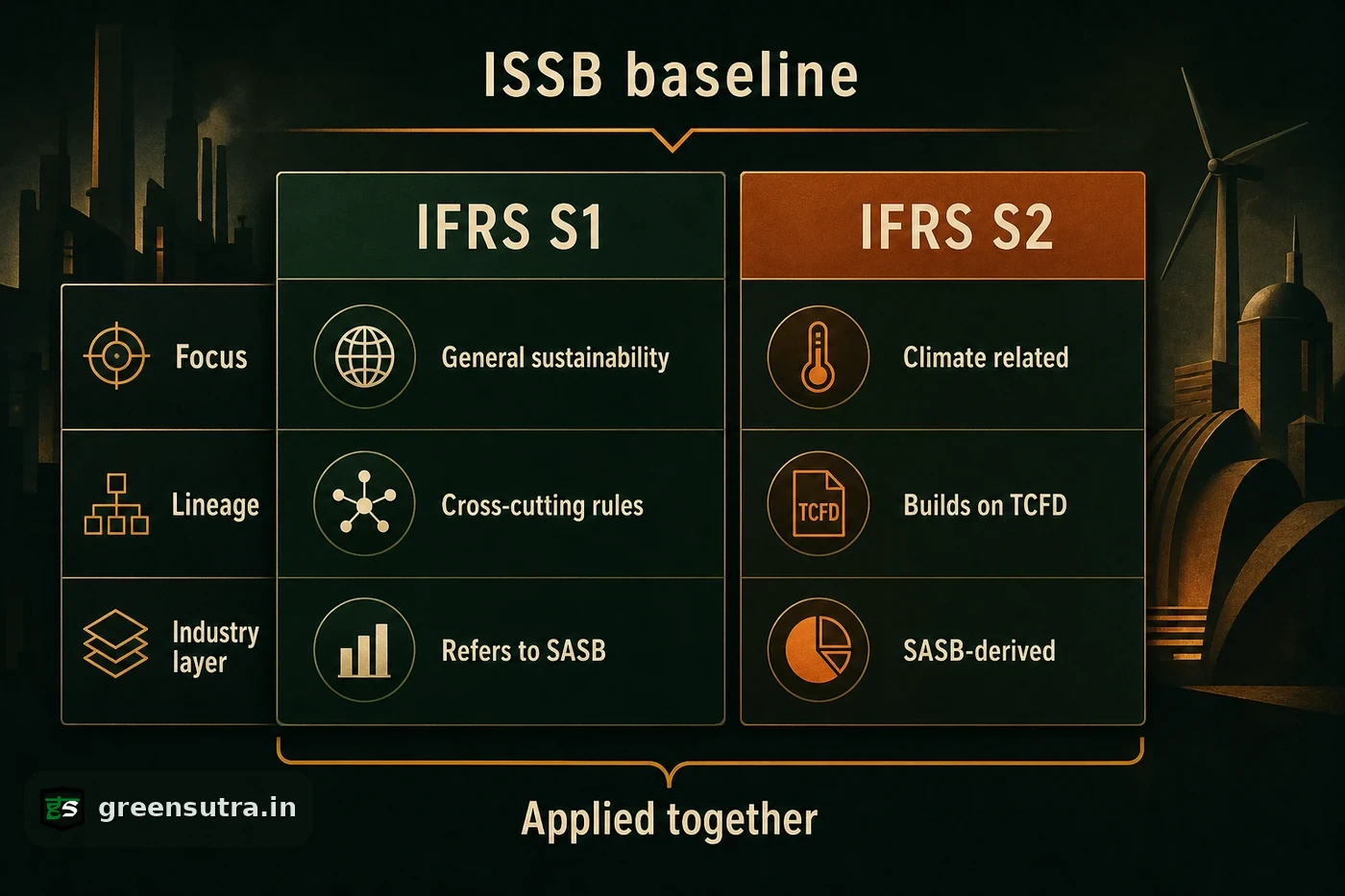

IFRS S1 versus IFRS S2

The two standards differ by scope, not by rigour, and are designed to be applied together.

| Dimension | IFRS S1 | IFRS S2 |

|---|---|---|

| Focus | General sustainability related financial information | Climate related disclosures |

| Lineage | Cross cutting disclosure requirements | Builds on the TCFD recommendations |

| Industry layer | Refers to the SASB Standards | Incorporates industry based requirements derived from SASB |

| Timing | Issued June 2023 | Issued June 2023 |

Two lineage points matter. Applying IFRS S1 and IFRS S2 together meets the TCFD recommendations, which are fully incorporated into the ISSB Standards, and monitoring of corporate climate disclosures transferred to the IFRS Foundation from 2024. The SASB Standards, now maintained by the ISSB following the Value Reporting Foundation consolidation on 1 August 2022, supply the industry based layer inside IFRS S2.

Who applies the baseline, and the BRSR touchpoint

The ISSB baseline applies to companies in jurisdictions that adopt or reference ISSB, and to exporters whose customers, investors or listing venues expect ISSB aligned reporting. Key applicability facts:

- IFRS S1: general sustainability related financial information for investors.

- IFRS S2: climate, including the industry based requirements derived from SASB.

- Adoption depends on each jurisdiction referencing the standards.

For Indian filers, the statutory BRSR format already gathers environmental, social and governance data; a single documented evidence base can then feed ISSB aligned climate reporting where investors expect it, avoiding duplicate collection. Independent accredited third parties provide any assurance over that data; the advisor readies and structures it. A short walk through the frameworks is in the ESG reporting guide.

Sources: IFRS Foundation, IFRS S2 · IFRS Foundation, TCFD responsibilities from 2024 · IFRS Foundation, SASB consolidation