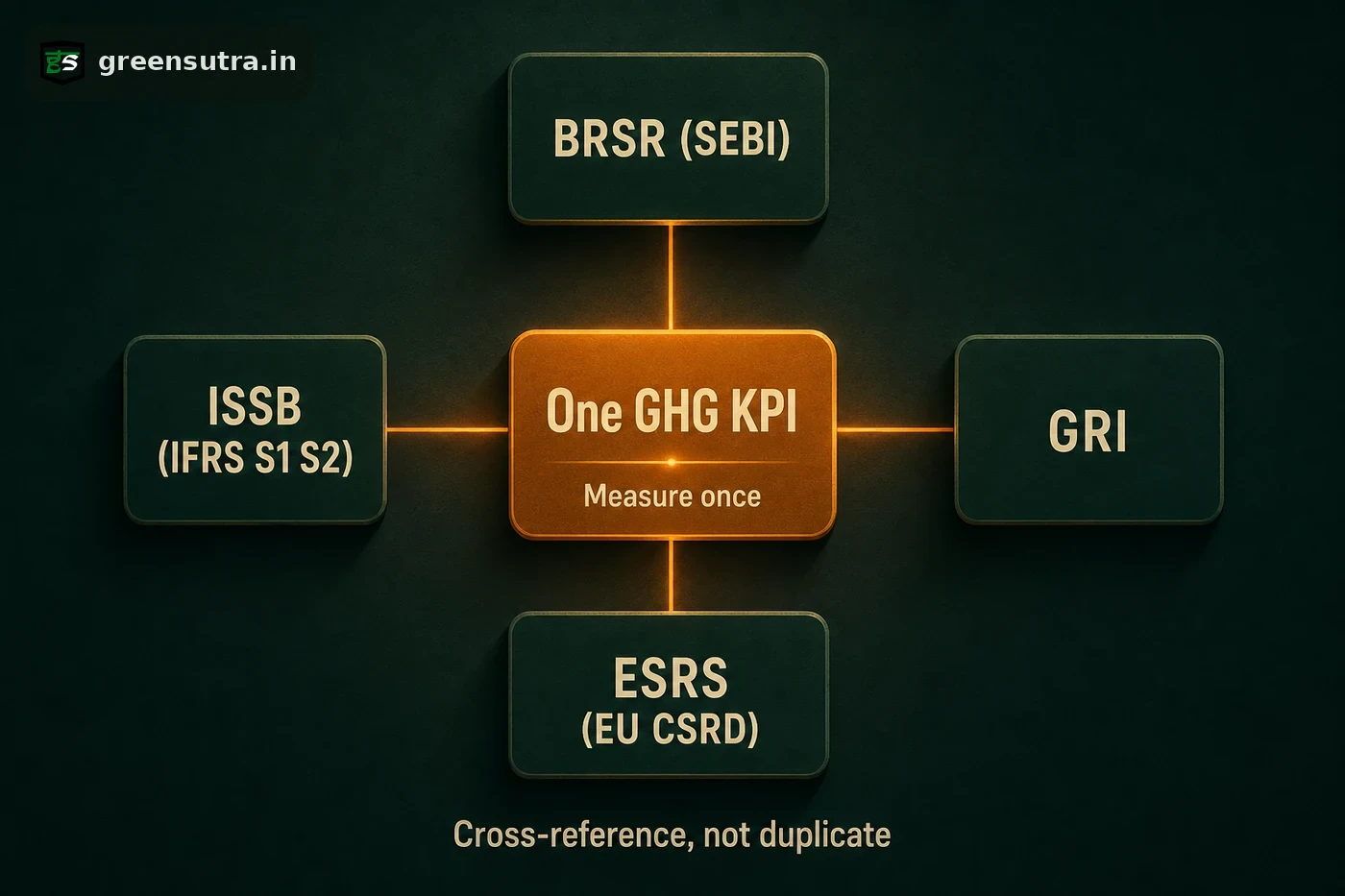

BRSR GRI ESRS mapping means cross-referencing one measured KPI, such as Scope 1 and Scope 2 GHG emissions, so the same figure satisfies SEBI’s BRSR, the GRI topic standards, the European ESRS under CSRD and the ISSB baseline in IFRS S1 and S2, avoiding duplicate data collection.

One measured KPI, four destinations

The Business Responsibility and Sustainability Report (BRSR) format, set by SEBI under Regulation 34(2)(f) of the SEBI (LODR) Regulations 2015, lets a listed entity already reporting under internationally accepted frameworks cross-reference those disclosures to the corresponding BRSR items rather than duplicate them. One measured figure, such as Scope 1 and Scope 2 GHG emissions, water consumption or energy consumption, can therefore feed several standards at once, provided the measurement boundary and methodology stay consistent.

- Measure the KPI once against a defined organisational boundary.

- Cross-reference the same figure to each framework’s indicator.

- Assure the figure once so it can be reused across reports.

How the frameworks line up

The same GHG figure lands in a distinct place in each framework, so mapping once keeps the numbers identical across every report:

| Framework | Applies to an Indian listed entity as | The Scope 1 and 2 GHG figure maps to |

|---|---|---|

| BRSR / BRSR Core (SEBI) | Statutory disclosure; top 1,000 by market cap from FY 2022-23 | GHG footprint attribute |

| GRI | Voluntary global standard | GRI topic standards |

| ESRS (EU CSRD) | Overseas-customer or group expectation | ESRS climate disclosures |

| ISSB (IFRS S1 and S2) | Investor or lender expectation, not mandated in India | IFRS S1 and S2 baseline, building on TCFD |

Assurance and market expectations

A cross-referenced dataset only holds value if the underlying figure is reliable. BRSR Core reasonable assurance, performed by independent accredited third parties, strengthens the same GHG figure that GRI, ESRS and the ISSB baseline all draw on. India has not mandated IFRS S1 or S2, so ISSB and TCFD alignment functions as an investor, lender or overseas-customer expectation rather than a domestic legal requirement. Full population of the essential and leadership indicators closes gaps that would otherwise weaken a downstream ESG rating issued by a SEBI-registered ERP. Building one clean dataset that answers all four frameworks is advisory work, and the ESG guide sets out the groundwork; the data file is readied for review while assurance stays with accredited third parties.

Sources: SEBI BRSR Core circular, 12 July 2023 · IFRS Foundation jurisdiction profiles