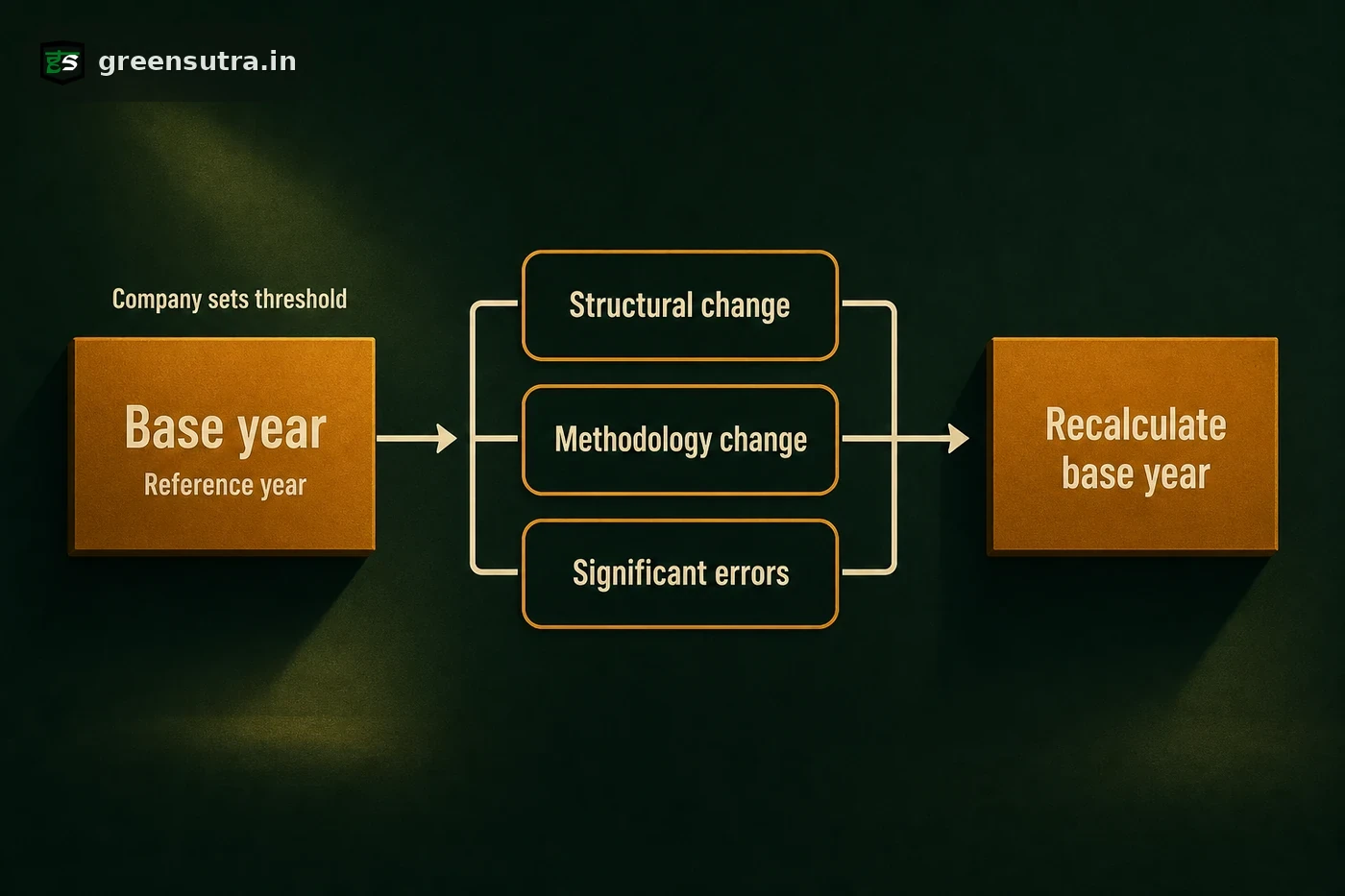

A carbon footprint base year is the reference year, chosen for a period with verifiable data, against which later emissions are tracked; the GHG Protocol Corporate Standard requires it to be recalculated after structural changes such as mergers, acquisitions or divestments, methodology changes, or the discovery of significant errors.

What a carbon footprint base year is

A base year fixes the point of comparison for a greenhouse gas inventory. It is the reference year against which emissions are tracked over time, chosen for a period with verifiable, representative data across Scope 1, Scope 2 and Scope 3. Once set, the base year anchors every later reduction claim, so its inventory must be documented thoroughly enough to support restatement years afterwards. Structured carbon footprint consulting establishes that baseline to the GHG Protocol Corporate Standard and keeps the supporting activity data auditable.

When a base year must be recalculated

The GHG Protocol Corporate Standard sets three conditions under which a base year is recalculated. A recalculation restates the base year and any intervening years, so the emissions trend stays comparable. Structural changes matter because they move emissions between inventories without changing what reaches the atmosphere.

| Trigger | What changes | Why recalculation is required |

|---|---|---|

| Structural change | Mergers, acquisitions, divestments, significant outsourcing or insourcing | Emissions transfer between organisations without altering total atmospheric output |

| Methodology change | New calculation methods, emission factors or improved data | Comparability with the base year would otherwise break |

| Significant errors | Discovery of material mistakes in the base year inventory | The reference figure must reflect corrected data |

Setting a significance-threshold policy

The standard makes no numerical recommendation for what counts as significant. Instead, each organisation sets, documents and discloses its own significance threshold in a base year recalculation policy. Some external programmes publish fixed figures as examples of practice, for instance a ten per cent threshold used by the former California Climate Action Registry, yet these are programme specific and are not a GHG Protocol default. A recalculation policy typically records:

- the significance threshold and how it is measured;

- the structural, methodology and error triggers that oblige a restatement;

- the treatment of corrected data once a base year is restated.

Setting this policy early keeps a footprint defensible and comparable. Further method detail sits in the carbon footprint guide, which walks through boundary setting and inventory preparation.

Sources: GHG Protocol Corporate Standard · GHG Protocol Corporate Standard, Chapter 5