Chinese aluminium is the most exposed under CBAM for two reasons. China is the largest in-scope EU supplier at EUR 3.9 billion, 13.1 percent of 2024 imports, because top-five peers Norway, Iceland and Switzerland are Annex III exempt, and China shows the highest estimated direct emissions intensity of the major routes, 2.28 tCO2e per tonne (Hasanbeigi/ORF 2025).

Volume: the exemption map leaves China on top

China is the largest aluminium supplier actually inside CBAM’s scope. Eurostat data for 2024 puts EU aluminium imports (HS 76) at about EUR 29.5 billion, and three of the five biggest suppliers sit outside the mechanism entirely: Norway, Iceland and Switzerland appear in Annex III of Regulation (EU) 2023/956 because they participate in the EU ETS or a linked emissions trading system. Once those three drop out, the repricing lands first on China, then on Türkiye.

| Supplier | 2024 EU imports | Share | CBAM status |

|---|---|---|---|

| Norway | EUR 4.4bn | 15% | Exempt (Annex III) |

| China | EUR 3.9bn | 13.1% | In scope |

| Türkiye | EUR 2.8bn | 9.4% | In scope |

| Iceland | EUR 2.1bn | 7.3% | Exempt (Annex III) |

| Switzerland | EUR 1.7bn | 5.8% | Exempt (Annex III) |

The full ranking is broken down in the EU’s top aluminium suppliers under CBAM, and the exemption logic in why Norway and Iceland escape CBAM on aluminium.

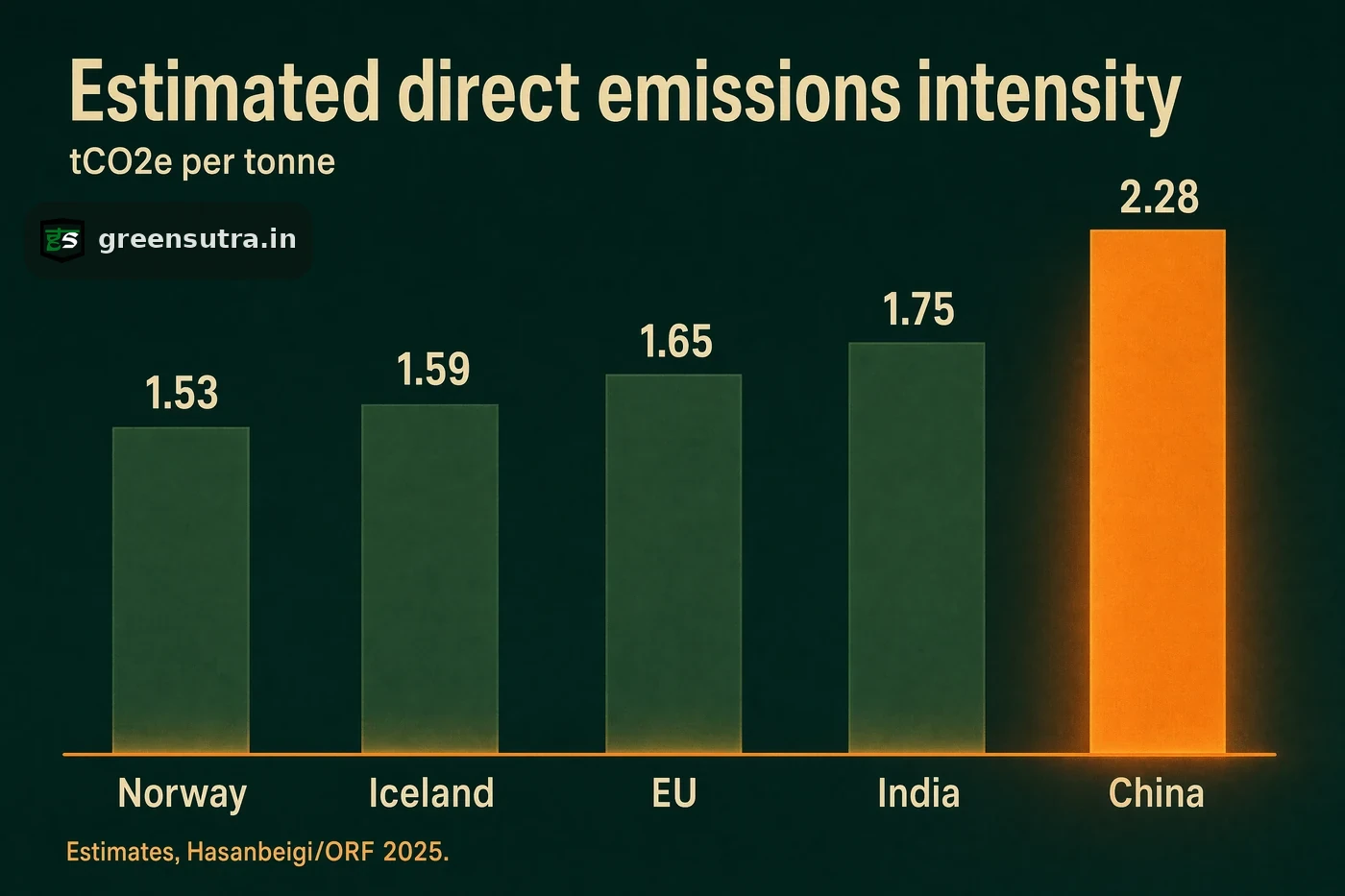

Intensity: the highest direct emissions of the major routes

Chinese primary aluminium also runs the steepest per-tonne carbon of the major supply routes. Hasanbeigi/ORF 2025 estimates put China at 2.28 tCO2e per tonne, against an estimated 1.60 to 1.65 for the Gulf producers, 1.65 for the EU and 1.75 for India; the exempt suppliers are also the cleanest, Norway at an estimated 1.53 and Iceland 1.59. One accounting nuance matters: aluminium is an Annex II good, so CBAM prices direct emissions only. The coal-heavy grid behind Chinese smelters adds nothing to the certificate obligation under the current scope. It is China’s direct smelting intensity, not its electricity mix, that is priced, and even on that direct-only basis Chinese metal sits well above every major competing route.

Implications for buyers and competing exporters

Buyers of Chinese metal shoulder the largest certificate exposure among the major origins, and the bill grows as the payable share climbs from 2.5 percent in 2026 to 100 percent by 2034.

- EU importers can model the position line by line in the CBAM cost calculator before renewing Chinese supply contracts, since volume and intensity land on the same invoice.

- Competing exporters in India and the Gulf hold a per-tonne advantage on paper; it becomes a declared advantage only when installation-level data replaces estimates and defaults and is verified by an accredited verifier.

- Preparing that data trail is consulting work: GreenSutra’s CBAM solutions service prepares importers and exporters for verification, which always sits with accredited verifiers.

Sources: Regulation (EU) 2023/956 · European Commission CBAM portal