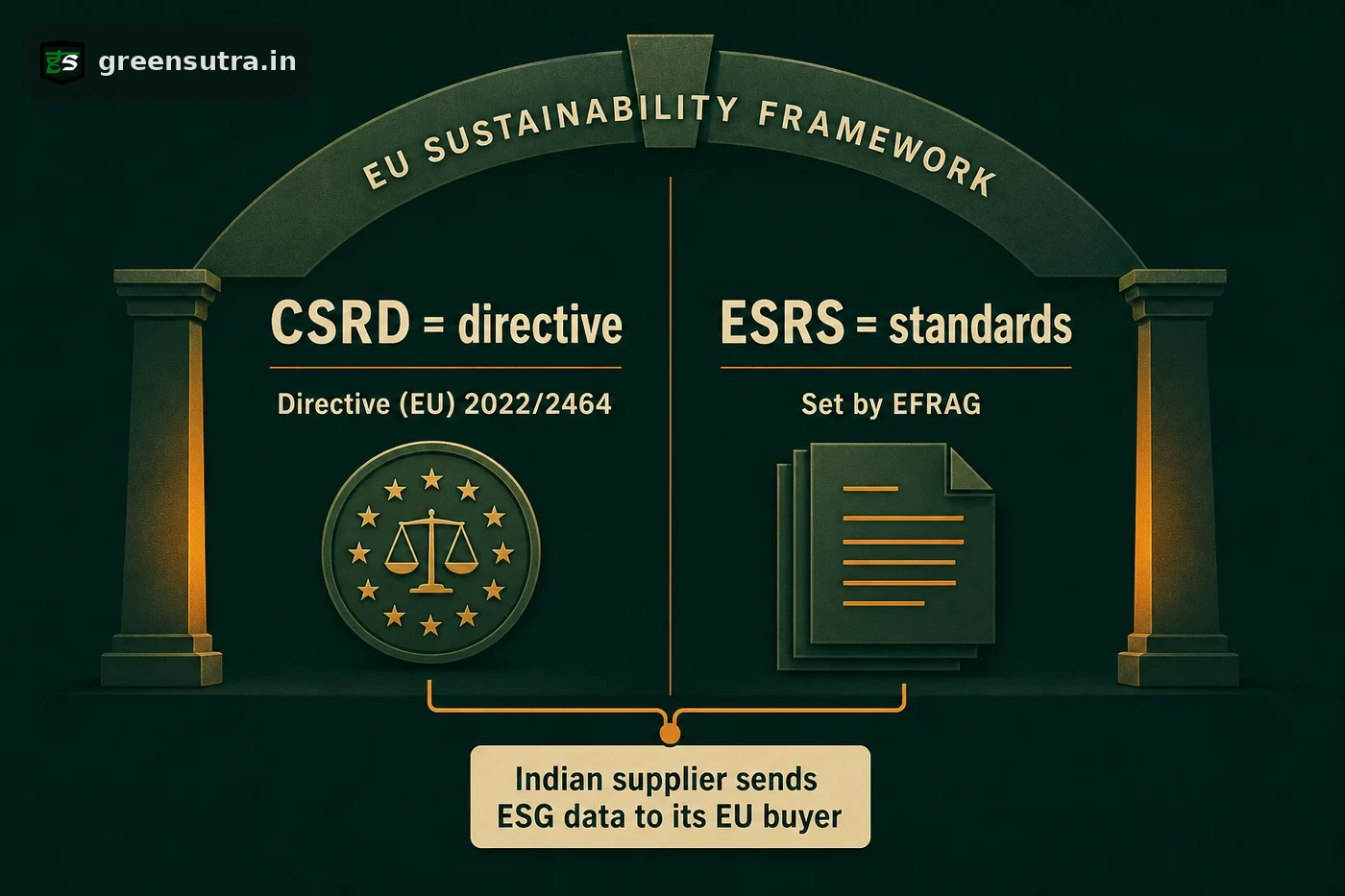

CSRD is the EU directive, Directive (EU) 2022/2464, that creates the reporting obligation; ESRS are the standards reported against under it, set by EFRAG on a double materiality basis. An Indian supplier below the third country thresholds files no ESRS report itself, and instead supplies the same environmental, social and governance data its EU customer requests to complete its own disclosure.

CSRD and ESRS are two different things

The distinction is straightforward once each term is placed correctly. CSRD is the law; ESRS are the standards written to satisfy it.

| Aspect | CSRD | ESRS |

|---|---|---|

| What it is | The EU Corporate Sustainability Reporting Directive, the law | The European Sustainability Reporting Standards, the reporting rules |

| Legal reference | Directive (EU) 2022/2464 | Standards used under the CSRD |

| Set by | European Union legislators | EFRAG |

| Function | Creates the obligation and defines who is in scope | Define what is reported and how, on a double materiality basis |

Double materiality means an entity reports both how sustainability issues affect its finances and how its own operations affect people and the environment.

When the directive reaches an Indian group directly

A third country group falls into CSRD scope only above specific thresholds, which the Omnibus I simplification narrowed. Omnibus I was published in the Official Journal on 26 February 2026 and came into force on 18 March 2026.

- EU net turnover above EUR 450 million in each of the last two consecutive years, and

- an EU subsidiary above EUR 200 million net turnover, or an EU branch above EUR 50 million.

The Member State transposition deadline is 19 March 2027, and reporting by non EU groups is expected to begin around financial year 2028. These thresholds and dates were still being transposed as of mid 2026, so they are the current but evolving position, subject to transposition and further simplification.

What a supplier below the thresholds reports

Most Indian suppliers sit below those thresholds and file no ESRS report of their own. The obligation still reaches them indirectly: an EU customer captured by the directive often asks its Indian suppliers for the same environmental, social and governance data needed to complete its own disclosure. The practical task is therefore a documented, assurance ready data file, not a formal filing. The ESG reporting guide sets out the frameworks in plain terms, an ESG discovery brief scopes the data gap, and the ESG solutions service prepares and readies the evidence base for independent verification by third parties.

Sources: Directive (EU) 2022/2464 · EFRAG sustainability reporting standards · European Commission, corporate sustainability reporting