SASB vs GRI marks a difference of audience and materiality direction, not quality: SASB Standards are investor focused, financially material and industry specific across 77 industries and now maintained by the ISSB inside the IFRS Foundation, whereas GRI Standards are impact focused, multi stakeholder and independent under the GSSB.

Two lenses, not two grades

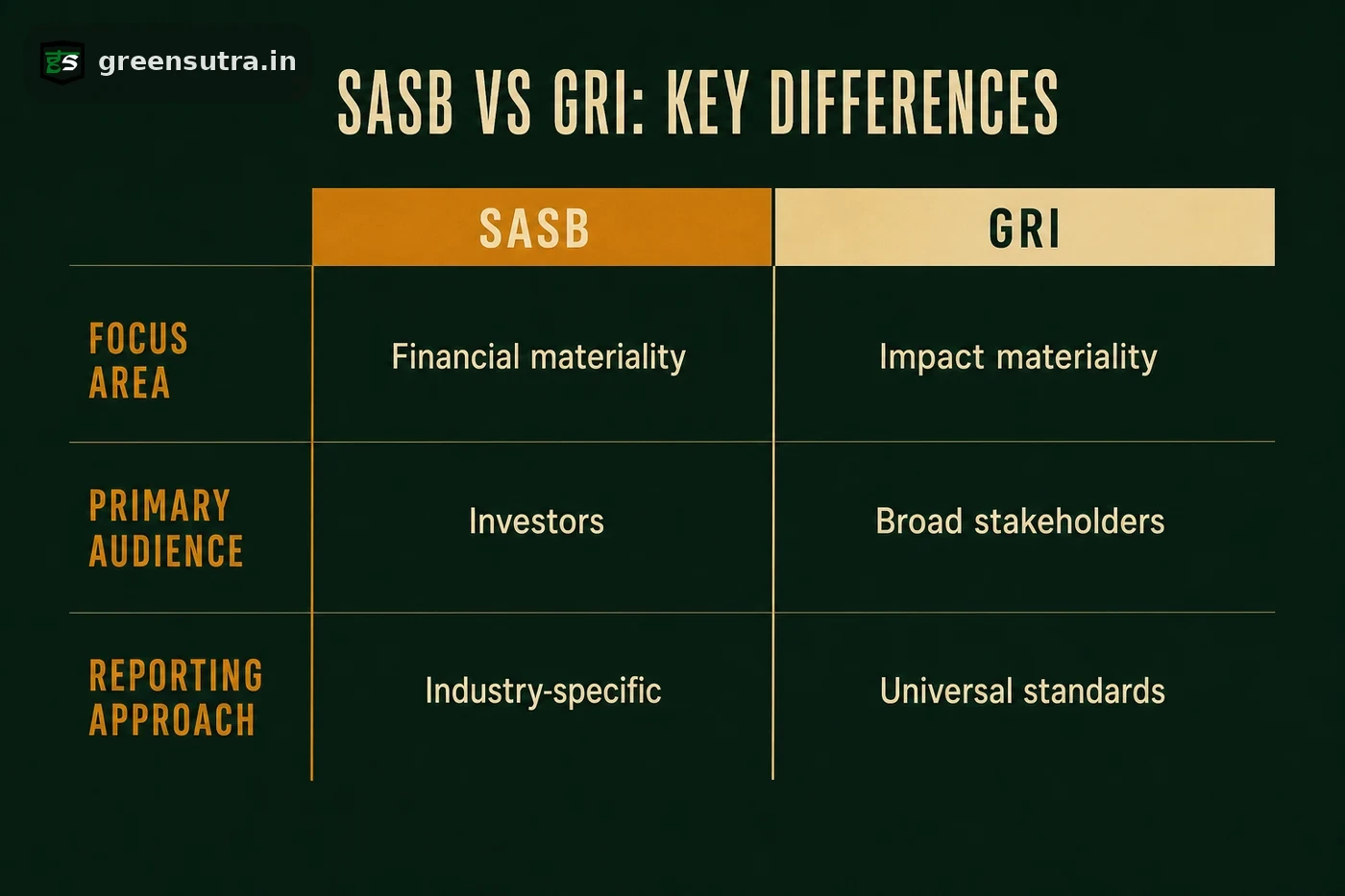

SASB and GRI answer different readers, and the gap is one of audience and materiality direction, not quality. The SASB Standards identify the sustainability related issues most relevant to investor decision making across 77 industries, so the materiality direction is financial, covering risks and opportunities that could reasonably affect a company’s cash flows, access to finance or cost of capital. The GRI Standards, set by the Global Sustainability Standards Board, are a modular, voluntary and free set of standards on an organisation’s impacts on the economy, environment and people, so the direction is impact and the intended readers are all stakeholders. Choosing between them, or running both, is part of framework selection inside ESG solutions.

- Audience: SASB serves investors; GRI serves the full range of stakeholders.

- Materiality direction: SASB is financially material; GRI is impact focused.

SASB vs GRI at a glance

The two standards line up cleanly on a handful of axes.

| Dimension | SASB Standards | GRI Standards |

|---|---|---|

| Audience | Investors | Multi stakeholder |

| Materiality direction | Financial | Impact |

| Structure | Industry specific, 77 industries | Universal, Sector and Topic standards |

| Nature | Investor focused disclosure | Voluntary and free |

| Custody | Maintained by the ISSB, IFRS Foundation | Independent, under the GSSB |

Where SASB now sits

The custody point is where drafts commonly err. SASB is no longer an independent standard setter. The Value Reporting Foundation, which held the SASB Standards, consolidated into the IFRS Foundation on 1 August 2022, and all open SASB projects transitioned to the ISSB on that date. The ISSB now maintains and enhances the SASB Standards, the same board that issued IFRS S1 and IFRS S2, while GRI remains separate under the GSSB. IFRS S2 also incorporates industry based disclosure requirements derived from the SASB Standards, so the industry specific content SASB built now sits inside the ISSB baseline. As of 2024, 77 percent of the world’s 250 largest companies report with GRI, a measure of how widely the impact lens is used. For an exporter deciding what to report and to whom, the ESG reporting guide sets out the frameworks, and a documented data file can be readied for independent verification by accredited third parties, which GreenSutra prepares but never performs.

Sources: IFRS Foundation (SASB Standards) · GRI Standards · GRI on global adoption by the largest companies