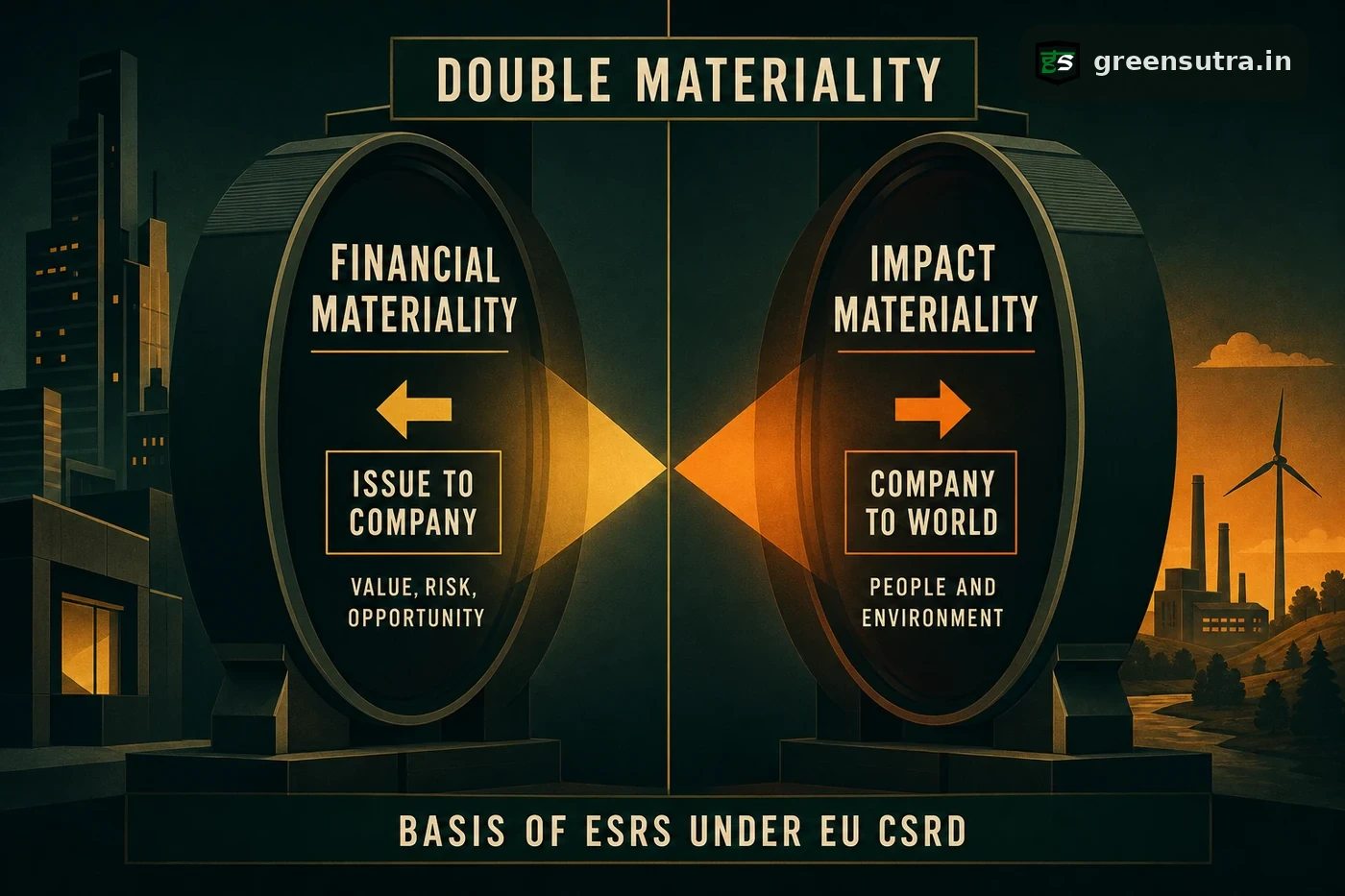

Double materiality is the ESG reporting principle that assesses two directions at once, financial materiality, meaning how a sustainability issue affects a company, and impact materiality, meaning how that company affects people and the environment, and it forms the basis of the ESRS under the EU CSRD.

Two directions assessed at once

Double materiality reframes a materiality assessment, which ranks the environmental, social and governance issues that matter most for a specific company, so that two questions are answered together rather than one. Financial materiality asks how a sustainability issue affects the company, its value, risk and prospects. Impact materiality asks how the company affects people and the environment. Both lenses run in parallel, and an issue can qualify under either or both. Structuring that assessment sits at the front of ESG solutions.

Financial materiality versus impact materiality

| Lens | Question asked | Focus |

|---|---|---|

| Financial materiality | How a sustainability issue affects the company | Value, risk and opportunity |

| Impact materiality | How the company affects people and the environment | External outcomes |

The dual test widens what a company must consider, because an issue overlooked on financial grounds can still be reportable on impact grounds. An issue rises to reporting relevance when it is material under at least one lens:

- Financially material only, such as a regulatory cost with a limited external footprint.

- Impact material only, such as a community effect with modest near term financial weight.

- Material under both, such as emissions, which carry environmental harm and carbon cost together.

The ESRS basis under the EU CSRD

The European Sustainability Reporting Standards (ESRS), set by the European Financial Reporting Advisory Group (EFRAG) and used under the EU Corporate Sustainability Reporting Directive (Directive (EU) 2022/2464), are built on a double materiality view of an entity’s impacts and its financial risks and opportunities. Companies in scope of the CSRD report against the ESRS. The directive can reach a non EU parent group through its EU operations, and even below its thresholds an EU customer captured by it often asks its Indian suppliers for the same ESG data, so a documented assessment matters ahead of any direct obligation. India’s own BRSR format serves a parallel statutory disclosure purpose for the country’s largest listed companies. A structured walkthrough sits in the ESG reporting guide.

Sources: EFRAG (ESRS) · Directive (EU) 2022/2464 (EUR-Lex)